"Companies that lack proper accounting controls or compliance processes could theoretically become public companies after only having to convince a small number of private investors that they are worthwhile investment risks. The general investing public, who lack insight into the behind-the-scenes process, could then invest in the not thoroughly vetted company via the SPAC's public offering." – Constantine

A Bloody History

During the 1980s and 1990s, this type of transaction was called a reverse public merger or reverse takeover with a blank cheque company.2 A company desiring to finance its operations was convinced that being public was precisely the key needed to get the money they needed. The public shell3 would have audited financial statements, a symbol, and would be trading publicly. Mind you, they may have been trading by appointment, but trading they were. As soon as the companies were merged, the private company shareholders would have 80% of the shares outstanding and the public company 20%. A minnow swallowing a whale – a nice trick if you can do it. The whole deal may have cost $50,000 to $125,000. Common problems are the private company's over-valuation, the repeated failure of the promised PIPE financing, and zero due diligence.

In the late 1990 and early 2000s, over 150 Chinese companies got instant U.S. listing by merging into a U.S. SPAC Company. The fad saw some $50 billion worth of these deals launch before investors learned that many of the China reverse-takeover firms were frauds. Their factories are fake. Their books cooked. The problem of a reverse takeover is that the apparent information asymmetry gives private companies a vast space to commit mischief, deceive themselves, or defraud the public. There was no 3rd party due diligence – period. That's right; $50 billion was lost – fleeced from investors in SPAC transactions.

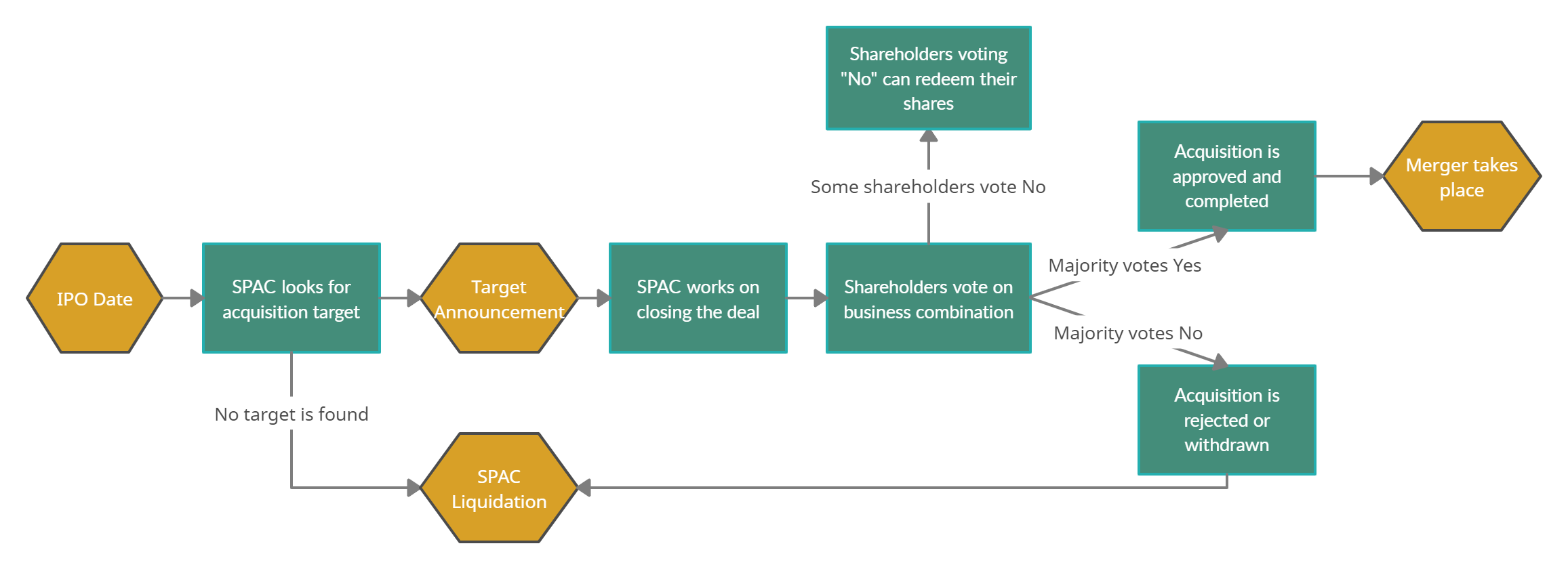

Around 2015, SPACs began to offer IPO investors 100% money-back guarantees, with interest; the holder would also be entitled to keep any warrants or special rights, even if they voted against the merger and tendered their shares. Even more significantly, they could vote yes to the union and still redeem their shares. In effect, this gave sponsors the green light on any merger partner they chose. It also made SPAC IPOs a no-lose proposition, effectively giving buyers a free call option on rising equity prices. As the Fed's low-rate, easy-money policy propelled the stock market higher for over a decade, it was just a matter of time before SPACs came back into vogue. And so they have, with unprecedented force.

Blank-check companies were created in the 1980s and were associated with fraudulent activity and penny stocks, which gave them a bad reputation. They now have stricter rules. The average size of a SPAC raised this year is more than $230 million, compared with about $180 million in 2016, the data showed. To be sure, SPAC listings come with risks. Target companies often give up more control and economics when they sell to a SPAC, which has its operating team in place. They're also subject to a vote by the SPAC shareholders. Sometimes this can lead to deals being scrapped before they can close.